(convert.io)")

Costs for continuing education have skyrocketed over the past several years, rising 40% in the past decade according to FINRA. In fact, based on that historical performance, ten years from now you can expect to pay over $62,000 for a four-year public college education, and most likely a considerably higher cost for a private university.

While this number seems daunting, the earlier you start saving for your child’s education, the greater chance you have of having enough put away to make a major dent in his or her college payments. Through smart planning choices and the rate of return you may get from investing appropriately, even a small amount put away each month can go a long way.

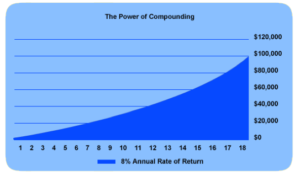

FINRA gives a great example here. If you save $200 per month at a 6% annual rate of return for your newborn child, you could have more than $76,000 for his retirement when he turns 18:

This example is for illustrative purposes only and the return is not indicative of any actual investment. Actual investment results may differ substantially.

When it comes to saving for your children’s or grandchildren’s education, the first thing you should always do it make an estimate and set a goal. When we work with our clients on their education savings plans, we usually ask the following questions:

- How many children do you want to send to college?

- Do you want to attempt to pay for college in full, or would you like your children to contribute to their own educations as well?

- What other major life events do you need to save for?

- How do your retirement savings accounts look?

While saving for college is important, we believe it should be just one element of a sound financial plan aimed at helping you achieve all of your financial goals, not just one. To learn more about how we help our clients create smart goals for their futures, please contact us. We’d love to hear from you!